Planning for the long-term financial well-being of a loved one with a disability isn’t just a challenge. For many Canadian families, it’s a deep source of stress. Questions like “What will happen when I’m gone?” or “Will they have enough?” linger for years without clear answers.

There’s a powerful solution that many Canadians haven’t yet discovered: the Registered Disability Savings Plan (RDSP).

The RDSP is a savings plan designed specifically for Canadians with disabilities. Contributions are not tax-deductible, but investment growth is tax-deferred which allows more of your money to stay invested over time.Most importantly, the RDSP comes with substantial government contributions.

To qualify, the beneficiary must:

This is a matching grant that can provide:

For families earning less than $111,733, a $1,500 contribution is enough to unlock the full $3,500 grant. Families with higher incomes qualify as well, but larger contribution may be required to maximize grants.

Lower-income families may also receive up to $1,000 per year in additional bonds, without needing to contribute anything!

You may be eligible to receive up to 10 years of unclaimed grants and bonds when opening an RDSP. This can result in a major boost in year one.

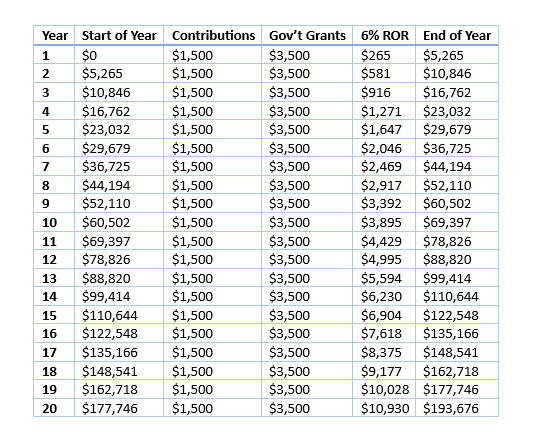

Let’s look at an example:

A family with $110,000 in annual income contributes $1,500 per year. Each year, the government also contributes $3,500. Assuming a 6% net rate of return, $30,000 of contributions (i.e. $1,500 per year multiplied by 20 years) could result in $193,676 in accumulated savings.

If you or someone in your family qualifies for the Disability Tax Credit, we can:

Despite its generous benefits less than 35% of eligible Canadians currently use an RDSP (according to the Government of Canada’s 2023 RDSP Statistical Review). That means most are leaving money on the table. Let's fix that!

📩 Reach out to Endeavour Wealth Management today and let’s build a plan that Safeguard’s your family’s future.

This information has been prepared by Ryan Secord who is a Senior Investment Advisor for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The Investment Advisor can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization. iA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operates.

If you felt a little uneasy at times this year, you weren't alone. It was a year characterized by mixed signals, economic data that defied expectation

December 29, 2025

Imagine you’re starting a road trip alone. You’ve got a full tank of gas, the music is on, the destination is… well, undefined. You could head toward

December 22, 2025

One of the core promises of index investing is diversification: own the market, spread your risk, and avoid reliance on any single company or sector.

December 15, 2025

Download your free guide to financial freedom.

Download your free guide to learn how you can protect your retirement savings with a Personal Pension Plan.

Download your free guide to help ensure you don’t run out of money.

Download your free guide to learn how to ensure your portfolio and plan stay on track.