Money touches almost every part of a relationship where you live, how you spend weekends, and what you say yes or no to. It’s also a leading source of conflict. The fix isn’t a complicated spreadsheet; it’s a structure you both understand and a simple habit of talking about it regularly. With a bit of planning, money can become a place of alignment rather than friction.

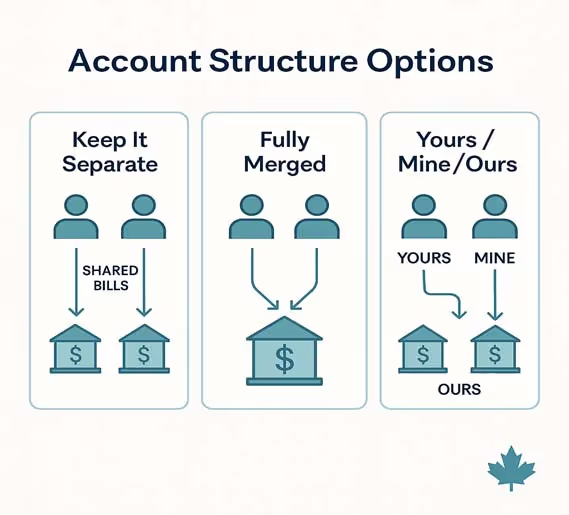

The first decision is how you’ll set things up together. Some couples keep everything separate and split shared expenses based on an agreed rule, either half and half, or in proportion to income. Others fully merge, pooling paycheques and paying all bills from joint accounts. Most people land in the middle with a “yours, mine, and ours” approach: you keep individual checking accounts for personal spending and open a joint account for shared costs like housing, groceries, insurance, and travel. Each partner contributes to the joint account on a schedule and keeps a reasonable amount of “no-questions-asked” money for their own purchases. If incomes differ, a proportional split usually feels fairer and reduces resentment. Whatever you choose, automate contributions so the essentials are covered before the fun spending happens.

A short monthly “financial date night” keeps you aligned without turning the relationship into a running tally of who owes what. Block forty-five minutes, put the phones away, and start with what went well this month. Take a quick pulse on cash flow, what came in, what went out, and whether you’re close to your savings target. Look at progress on the things that matter: an emergency fund, debt repayments, and topping up RRSPs, TFSAs, or an FHSA if a first home is on the horizon. Flag any bigger expenses coming up so they don’t surprise you later. If one of you is considering a larger purchase, agree on an approval threshold that requires a check-in beforehand. End on a positive note by naming one thing you’re excited to fund this year. If emotions spike, press pause and pick it up again tomorrow money talks work best when they’re calm and predictable.

Different money personalities don’t have to be a problem. In many relationships, one person leans “saver” and the other “spender.” Those tendencies can complement each other if you treat them as strengths: the saver protects your future, and the spender makes sure you actually enjoy today. Give each person a set amount of personal spending room every month so small choices don’t become debates. For impulse-prone purchases, try a 24-hour buffer before buying. Divide roles in a way that plays to your strengths perhaps one person leads the day-to-day bill payments and cash-flow check-ins while the other handles investment admin and insurance renewals and swap roles once a year so you both stay informed. Automate as much as you can so your conversations focus on goals and trade-offs rather than transactions.

A Canadian lens adds a few valuable tools. If your retirement incomes are likely to be uneven, a spousal RRSP can help balance things out. One partner contributes to an RRSP in the other partner’s name and receives the tax deduction, while the receiving partner owns the account; over time, that can even out retirement income and reduce total tax. Just be mindful of attribution rules when withdrawals made within carefully, especially around retirement or parental leave.

Pension income splitting is another lever to plan around. In retirement, you may be able to allocate up to 50% of eligible pension income to a spouse for tax purposes. Before age 65, that typically means lifetime pension income from a defined benefit plan; after 65, RRIF or LIF withdrawals often become eligible (unlike RRSP withdrawals before conversion). CPP pension sharing is a related option couples can apply to share CPP retirement benefits based on years lived together. All three aim at the same goal: smoothing taxable income across the household to potentially lower total tax and reduce OAS claw-backs.

TFSAs deserve a special mention. They’re individual accounts, but you can gift money to your partner to contribute to their TFSA without triggering attribution, which makes them a powerful way to build tax-free balances on both sides. With non-registered investing, gifting is trickier because income or gains can be attributed back to the higher-income spouse; if you plan to invest gifted funds outside registered accounts, get advice so you don’t accidentally undermine the benefit you’re aiming for. If kids are in the picture (or may be soon), a family RESP lets you pool contributions and share CESG grant room among beneficiaries, which is helpful when siblings move through school at different times. And don’t forget the legal backdrop: rights and obligations differ by province and by marital versus common-law status. If you’re entering the relationship with significant assets or debts, or you’re common-law, it’s sensible to get legal advice on a cohabitation or prenuptial agreement clarity now is much cheaper, financially and emotionally, than conflict later.

To make this real, keep it simple. Many couples thrive with a hybrid setup one joint chequing account for shared bills, one joint savings account for shared goals, and individual accounts for personal spending. Automated transfers handle the heavy lifting; your monthly date night keeps you aligned on the big picture. As your situation evolves, layer in spousal RRSPs to balance retirement income, consider pension income splitting and CPP sharing in your withdrawal plan, and keep filling TFSAs on both sides. Revisit the rules once a year and adjust as incomes, goals, or family needs change.

The bottom line is straightforward: you don’t need perfect spreadsheets to have a healthy money life together. You need a structure you both trust, a short, repeatable conversation, and a plan that respects your differences while aiming at the same goals. Start small, automate where you can, and keep talking

Mitchell Cathcart, Marketing Assistant, Kondwelani Kalinda, Associate Investment Advisor and Grant White, Portfolio Manager at Endeavour Wealth Management with iA Private Wealth, an award-winning office as recognized by the Carson Group. Together, Endeavour Wealth Management provides comprehensive wealth management planning for business owners, professionals and individual families.

This information has been prepared by Mitchell Cathcart Marketing Assistant, Kondwelani Kalinda, Associate Investment Advisor and Grant White, Portfolio Manager for iA Private Wealth and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The Investment Advisor can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and Canadian Investment Regulatory Organization. IA Private Wealth is a trademark and business name under which iA Private Wealth Inc. operate

A net worth statement is often viewed as a simple calculation: what you own minus what you owe. While that number is important, it does not tell the..

June 8, 2026

For decades, retirement followed a fairly predictable formula. You worked full-time for most of your adult life, retired around age 65, and then final

June 1, 2026

Running a business in Canada is a bit like paddling a canoe across Lake Winnipeg in October it’s rewarding, but the conditions can change fast....

May 25, 2026

Download your free guide to financial freedom.

Download your free guide to learn how you can protect your retirement savings with a Personal Pension Plan.

Download your free guide to help ensure you don’t run out of money.

Download your free guide to learn how to ensure your portfolio and plan stay on track.