For many Canadian business owners and investors, 2025 ended with a sigh of relief. The high-profile reversal of the capital gains inclusion rate hike felt like a victory for capital preservation. However, as we settle into 2026, a new "shadow" tax system has fully emerged from the wings: the revised Alternative Minimum Tax (AMT).

While the inclusion rate stayed at 50%, the AMT rules have been quietly rewritten. If you are planning a significant asset sale, exercising stock options, or making a major charitable impact this year, the "standard" tax calculation is only half the story.

The AMT is a parallel tax calculation that prevents high earners from using certain deductions and lower tax rates to pay little to no tax. You essentially calculate your taxes twice: once under the Regular System and once under the AMT System. You pay whichever is higher.

In 2026, three specific "levers" have made the AMT a primary concern for the upper-middle class:

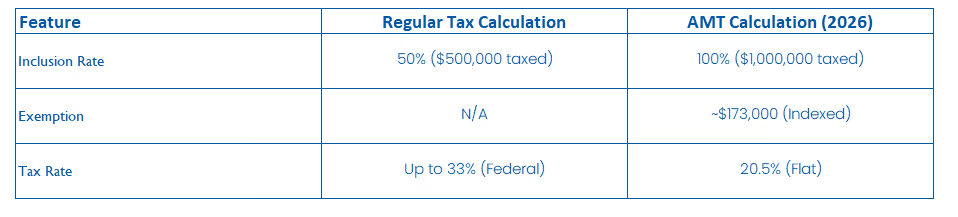

To understand the impact, let’s look at a hypothetical business owner in Winnipeg realizing a $1,000,000 capital gain from the sale of a property or non-qualified shares.

In this scenario, the AMT system may view your "taxable income" as significantly higher than the regular system does. If your AMT exceeds your regular tax, the difference is an additional payment you must make today.

The Silver Lining: AMT is technically a "pre-payment." You can carry the extra tax paid forward for seven years to offset regular taxes in the future. However, this creates a significant "liquidity drag"—money that could be invested in your business or portfolio is instead sitting with the CRA as an interest-free loan.

At Endeavour Wealth Management, we believe that tax is a structural challenge, not just a year-end filing task. To manage the 2026 AMT impact, we are focusing on three architectural pivots:

The 2026 tax landscape rewards the proactive. The days of "simple" tax planning are over; we are now in an era of integrated wealth architecture. If you are expecting a significant financial milestone this year, the time to model your AMT exposure is now not next April

This information has been prepared by Brandt Butt who is an Investment Advisor and Portfolio Manager for iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained in this newsletter comes from sources we believe reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation dating from the date of publication and are subject to change without notice. Furthermore, they do not constitute an offer or solicitation to buy or sell any of the securities mentioned. The information contained herein may not apply to all types of investors. The Investment Advisor and Portfolio Manager can open accounts only in the provinces in which they are registered.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization. iA Private Wealth is a trademark and a business name under which iA Private Wealth Inc. operates.

There are few moments in life more difficult than losing someone you love. In the days and weeks that follow, families are often navigating grief, fun

June 22, 2026

A net worth statement is often viewed as a simple calculation: what you own minus what you owe. While that number is important, it does not tell the..

June 8, 2026

For decades, retirement followed a fairly predictable formula. You worked full-time for most of your adult life, retired around age 65, and then final

June 1, 2026

Download your free guide to financial freedom.

Download your free guide to learn how you can protect your retirement savings with a Personal Pension Plan.

Download your free guide to help ensure you don’t run out of money.

Download your free guide to learn how to ensure your portfolio and plan stay on track.