In April 2011, a famous author warned that a catastrophic stock market crash was coming. He has repeated that warning, with conviction, almost every year since. One day he may even be right. But an investor who heeded him and stepped aside in 2011 missed a U.S. market that went on to return roughly 280 percent.

That's the uncomfortable arithmetic of doom. This June, the warnings are loud again: Jim Grant is calling AI one of the great bubbles of all time, Jim Chanos notes that AI spending now dwarfs the dot-com build-out, Ray Dalio has described this market as “classic bubble stuff” and is forecasting negative real returns for a decade. Ben Carlson of Ritholtz Wealth Management recently in his blog made the point that legends like Dalio and Jeremy Grantham have been issuing versions of these warnings for ten years and counting. The problem however is for most investors; the real damage usually isn't the bubble. It's what acting on the bubble call does to your money over the long-term.

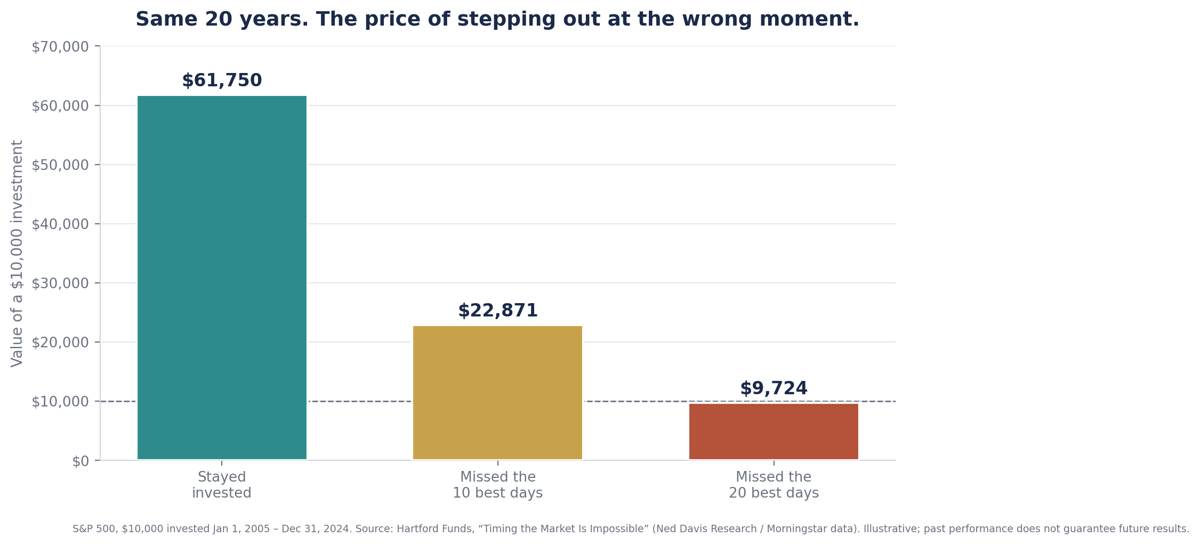

Suppose in 2011, you grew nervous, sold, and waited for a better entry point. The problem is that nobody rings a bell, and the market's best days have a cruel habit of arriving right in the middle of the scary ones. A $100,000 investment in the S&P 500 left untouched from 2005 through 2024 grew to about $617,750. Miss only the ten best days over those two decades — ten days out of roughly five thousand — and you end with $228,710. Miss the twenty best, and you're below where you started.

Why is this so punishing? Because seven of the ten best days over that period landed within two weeks of the ten worst days. The crash and the rebound are practically neighbours. To dodge the bad days you have to be out, and being out is exactly how you miss the good ones. The investor who “correctly” sensed danger and the investor who quietly did nothing can end up worlds apart.

It's tempting to think the answer is simply better forecasters. It isn't. Over the 25 years from 2000 through 2024, Wall Street's consensus predicted a market gain every single year — even though stocks actually fell in seven of them — and the average annual forecast missed the real result by more than 14 percentage points. These are full-time professionals with every resource imaginable. The lesson isn't that the bears are foolish and the bulls are wise. It's that the future genuinely isn't knowable in advance, so building a plan that depends on predicting it is building on sand.

Most investors think they have two choices: dismiss the bubble talk and ride whatever's hot (like AI), or believe it and bail out. We think there's a better one, and it's the foundation of how we invest at Endeavour Wealth Management — an evidence-based approach grounded in the same Nobel Prize-winning research utilized by Dimensional Fund Advisors.

It starts with broad global diversification — owning thousands of companies across many countries instead of crowding into the handful of names currently in fashion. That alone means you participate in the AI for as long as it continues running. But without your future hinging on it. We then apply a deliberate, modest tilt toward the characteristics that decades of research link to higher expected long-term returns: smaller companies, companies priced cheaply relative to their fundamentals (value), and highly profitable companies. These factors come from the work of Eugene Fama and Kenneth French, whose five-factor framework adds profitability and investment to the classic market, size, and value factors.

Here's the quiet elegance of it. Because you're diversified, you still own the winners of any boom. But because you tilt toward value and profitability, you are structurally underweight the most expensive, most speculative, least profitable stocks precisely the ones that fall hardest when enthusiasm fades. You hold the upside and a built-in shock absorber at the same time, and you never had to predict when, or whether, the music stops

You will hear someone declare this is the top. As the saying goes, a broken clock is right twice a day. Eventually, market bears will be right. But you don't get rich being scared at the correct moment — you get rich by owning great businesses through the tops, the bottoms, and the long, unglamorous middles. A globally diversified, evidence-tilted portfolio is built to do exactly that. It's less thrilling than calling the crash. It's also a great deal more reliable.

• Ben Carlson, “Spotting Bubbles and Calling Tops,” A Wealth of Common Sense (June 21, 2026).

• Hartford Funds, “Timing the Market Is Impossible” (Ned Davis Research / Morningstar data, 2005–2024).

• U.S. News & World Report, “Robert Kiyosaki’s Track Record on Predicting Stock Market Crashes.”

• Daner Wealth, “The Terrible Track Record of Wall Street Forecasts.”

• Eugene F. Fama & Kenneth R. French, “A Five-Factor Asset Pricing Model,” Journal of Financial Economics (2015).

• Benjamin Felix / PWL Capital, “Five-Factor Investing with ETFs” and the Rational Reminder podcast.

The information on this page was prepared by Brandt Butt, who is a Investment Advisor and Portfolio Manager with iA Private Wealth Inc. and does not necessarily reflect the opinion of iA Private Wealth. The information contained on this page is taken from sources we consider reliable, but we cannot guarantee its accuracy or reliability. The opinions expressed are based on an analysis and interpretation as of the publication date and may change without notice. Furthermore, they do not constitute an offer or a solicitation to buy or sell the securities mentioned. The information contained herein may not be suitable for all types of investors. iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization. iA Private Wealth is a trademark and trade name under which iA Private Wealth Inc. carries on business.

iA Private Wealth Inc. is a member of the Canadian Investor Protection Fund and the Canadian Investment Regulatory Organization. iA Private Wealth is a trademark and a business name under which iA Private Wealth Inc. operates.

There are few moments in life more difficult than losing someone you love. In the days and weeks that follow, families are often navigating grief, fun

June 22, 2026

A net worth statement is often viewed as a simple calculation: what you own minus what you owe. While that number is important, it does not tell the..

June 8, 2026

For decades, retirement followed a fairly predictable formula. You worked full-time for most of your adult life, retired around age 65, and then final

June 1, 2026

Download your free guide to financial freedom.

Download your free guide to learn how you can protect your retirement savings with a Personal Pension Plan.

Download your free guide to help ensure you don’t run out of money.

Download your free guide to learn how to ensure your portfolio and plan stay on track.